People choose to take out horse insurance for several reasons, often to have cover for the unexpected. As we know, horses are naturally curious creatures and if left to their own devices can get into all sorts of mischief, which is why horse insurance can give you peace of mind.

However, while we know that reading your policy wording isn’t the most exciting of activities, it’s important to understand exactly what your insurance policy covers your horse for. Depending on the type of cover you select, there may be general exclusions you aren’t aware of, among other requirements, should you need to make a claim.

To get you started, we’ve detailed six of the common insurance mistakes you might unknowingly be making.

1. Making a Claim Within 14 Days

You may be under the assumption that when you take out a new horse insurance policy you have immediate protection. However, some horse insurance providers have a 14-day exclusion period where claims for illnesses or conditions are not covered.

What is covered?

- During the 14-day period most policies cover claims for injuries caused by an accident.

What is not covered?

- Costs for any illness or condition displaying clinical signs within 14 days of your policy first starting, or any illness or condition that develops from them.

Purpose of exclusion period

As we know, an illness or condition can sometimes come out of nowhere and take us by surprise. However, the reasons horse insurers adopt a waiting period are:

- To avoid taking on horses that are either already poorly or have a higher risk of developing illnesses that could lead to a higher volume of claims.

- It also helps to discourage fraudulent claims where horses have pre-existing conditions.

It’s worth considering to have horse insurance in place from the day you purchase your horse, that way you get the waiting period out of the way and have the cover you need for peace of mind.

2. Non-Disclosure

An insurance policy is a contract agreement between the policyholder (you) and the insurance company. When taking out an insurance policy you are required to provide accurate information so that the insurer can assess any risks and determine your insurance premium and coverage.

Failing to disclose relevant information, such as pre-existing conditions or even a minor injury, could lead to your policy becoming invalid.

For example: your policy includes vet’s fee’s cover, so when you make a claim, you’ll be required to provide a fully completed claim form, detailed veterinary report and complete medical history. This would highlight any previous injuries, illnesses or conditions that should have been declared and could result in your claim being rejected, policy cancellation or reduced coverage.

The best course of action is to remain transparent at all times with your insurer to avoid any misunderstandings.

3. Type of Use

Similar to making sure you disclose any previous injuries, illnesses or conditions, you will be required to specify your horse’s type of use.

Your horse’s type of use impacts your insurance coverage and premium; for example, a horse that is used for hunting or polo may be at a higher risk of injury than a horse that is used for hacking or as part of a riding club.

If your horse sustains an injury or manifests an illness or condition that happened whilst taking part in, or preparing for, an activity not included within your specified type of use, it might not be insured. This same exclusion would impact those who choose to have ‘loss of use’ cover.

4. A Safe Environment

It may seem obvious but it’s important to consider the suitability of the field or paddock where your horse has turnout time; specifically, the type of fencing you use to keep your horse secure. Some insurers will have a general exclusion for claims if a horse sustains an injury in a field that has barbed wire, stock fencing or plain wire fencing.

The reason for this exclusion is that it is viewed as a preventable risk, and the responsibility is on the owner to ensure that a duty of care has been taken. It could impact claims relating to equine mortality, vet’s fees, and loss of use.

5. Overvaluing Your Horse

Something that’s all too common with equine insurance is owners overvaluing their horses. It’s similar to thinking about how a car might depreciate in value the older it gets. Claims for ‘death, theft or straying’ will either be paid 100% of the sum insured OR its market value, whichever is less, and this is what often confuses owners.

While you may have paid £12,000 when you bought your horse at 4 years of age, it doesn’t mean two years on it is still worth that much. Furthermore, you could be paying a higher premium on your insurance if you continue to value the horse above its market value.

6. The Risk to Not Insure

Horse insurance is a big consideration, and it ultimately comes down to you thinking about how you might pay for the unexpected. As we’ve said before, no-one can predict when their horse might injure itself or become sick with a chronic condition – there’s no ‘on the spot insurance’ for these situations.

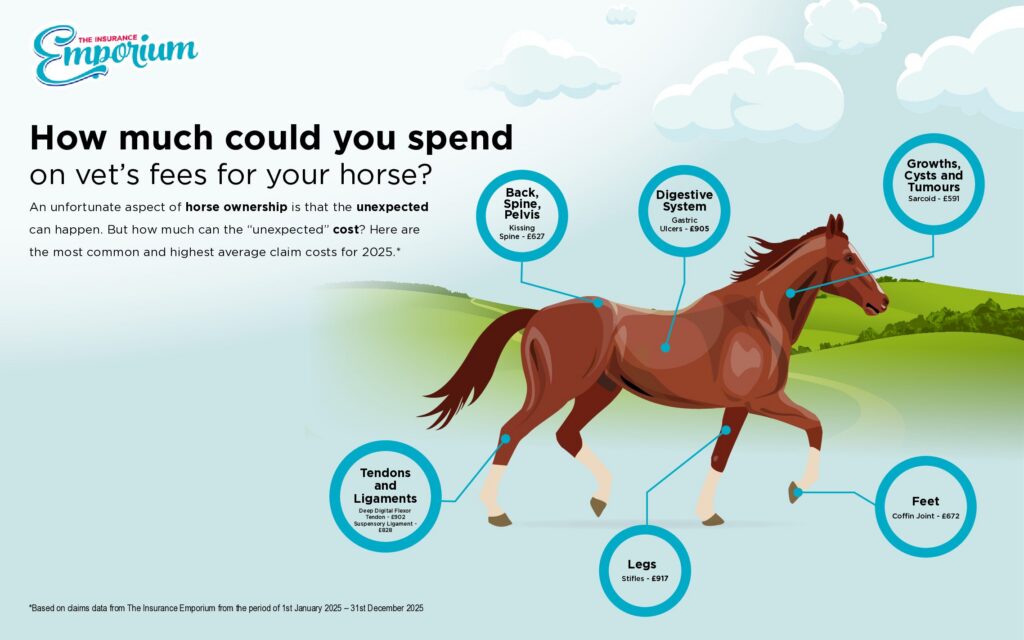

To help, we’ve put together some data* on the most popular claims alongside the most expensive claims, to give a rough idea of how much vet’s fees can be for unexpected illnesses and injuries.

Back, Spine, Pelvis

- Highest average claims value and most common claim – Kissing Spine – £579

Digestive System

- Highest average claims value and most common claim – Gastric Ulcers – £898

Growths, Cysts, Tumours

- Highest average claims value – Sarcoma and Hemangiosarcoma – £1,069

- Most common claim – Undiagnosed Mass – £590

Tendons and Ligaments

- Highest average claims value – Annular Ligament – £1,017

- Most common claim – Hind Limb Suspensory – £749

Legs

- Highest average claims value – Fetlock – £916

- Most common claim – Stifles – £858

Feet

- Highest average claims value – Multiple Conditions – £797

- Most common claim – Coffin Joint, Distal Interphalangeal Joint – £733

Horse insurance could give owners the peace of mind that should something go wrong, they have cover in place, leaving them to focus on their horse’s health and wellbeing. However, it’s always important to understand what your policy covers your horse for, as we’ve discussed, to avoid one of the common mistakes that might affect you if you need to make a claim.

Our horse insurance policies come with Death, Theft or Straying as a standard benefit, you can then tailor your policy with several additional optional benefits including Vet’s Fees, Loss of Use, and Personal Accident to match your needs. Take a look and get a free, no-strings quote today!

Watch Our Customer Testimonial

*Data provided is based on The Insurance Emporium’s own claims data from 2024 (1st Jan to 31st Dec).

All content provided on this blog is for informational purposes only. We make no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. We will not be liable for any errors or omissions in this information nor for the availability of this information. We will not be liable for any loss, injury, or damage arising from the display or use of this information. This policy is subject to change at any time.

We offer a variety of cover levels, so please check the policy cover suits your needs before purchasing. For your protection, please ensure you read the Insurance Product Information Document (IPID) and policy wording, for information on policy exclusions and limitations.